Welcome to my Pink Money Series! Just as companies rebrand ordinary objects into pink ‘women-friendly’ alternatives, the Pink Money Series is where I explain money information with feminine colors so women know ‘it’s for us.’

Gen Z Money

What do eating Tide-Pods and wealth-building have in common? The absence of fear. Sure one will land you in the hospital while the other on a beach in Aruba in early retirement, but nevertheless, Gen Z is fearless and they won’t take any of your shit.

As a Wealth and Wanderlust Educator, I couldn’t help but notice that my statistics on Gen Z were lacking BIG TIME. 100% of my Youtube Videos are watched by Millennials or older, but I still want to reach Gen Z as they have the most potential because they have the most TIME.

Where the young people at? Tik Tok I assume… so now I’m on Tik Tok.

Along with my quirky videos on Tik Tok, I also wanted to break down the basics for Gen Z on what personal finance tools are available to them. They will be the same as for anyone else… but with the added benefit of time.

You – my young friends – can potentially retire far younger than your predecessors. Myself include. Here’s how.

Gen Z Money Basics

In this article, you’re going to learn about:

- How and WHY you should set up an Emergency

- The benefits of a High-Yield Savings Account

- How to have $50,000 in your bank account by your 30s

This isn’t rocket science. This is math and Gen Z has TIME. Let me show you how you can set yourself up for success moving forward!

Need Help?

If you’re just starting out on your journey, check out my Beginner’s Budget Dashboard. It’s a Google Sheets template that tracks your expenses, income, investments, savings, and more! There’s even a free video tutorial to help you get started.

Build an Emergency Fund

Before we get into any of the complicated (but fun!) stuff, I cannot emphasize ENOUGH about the importance of building an Emergency Fund.

An emergency fund is a bank account with money set aside to cover large, unexpected expenses.

These unexpected expenses could be:

- Unemployment

- Unforeseen medical expenses

- Home Repairs

- Appliance Repairs or Replacement

- Car Repairs

- Etc

Basically, it’s to cover crappy shit that you didn’t expect to happen. An EF prevents you from going further into debt by covering unexpected expenses in cash, instead of with dangerous payday loans, etc…. This is NOT your Spring Break Holiday Fund.

Considering we’re in a global pandemic, why not stay at home and build your Emergency Fund while living at your parent’s house? No tea, no shade. This is an EXCELLENT way to stack cash fast.

Read my article on Emergency Funds.

Open a High-Yield Savings Account

Next, you should house your Emergency Fund in a High-Yield Savings Account (HYSA). This is the easiest way to help your money grow with as little risk as possible!

A HYSA is an account with a generous interest percentage that is paid to you as the bank customer to say ‘thanks for keeping your money here.’ Typically, savings accounts are crazy low with a 0.01% interest rate… and this is why you have to go hunt out HYSA the hard way.

If you don’t have your money in a HYSA, you are literally missing out on FREE money. Here’s why:

- Scenario 1: If you put in $10,000 into a HYSA with a 1.5% Interest Rate and continue to add $100 per month for 5 years. You’ll have just over $17,000 in your bank account in 5 years.

- Scenario 2: If you put $10,000 into a normal savings account with a 0.01% Interest Rate and continue to add $100 per month for 5 years. You’ll have just over $16,000 in your bank account in 5 years.

If you DON’T have your money in a HYSA, you’re missing out on FREE, virtually risk-free money. These accounts are ALSO typically insured up to a certain amount so sleep soundly knowing your money is taken care of.

Invest $200 a Month

Once you have the basics down, the natural next step is to start investing. Have you heard the good word about Compound Interest?

Compound Interest is the addition of interest to the original sum of your investment – aka, interest on interest. This happens when you reinvest the interest of your investments.

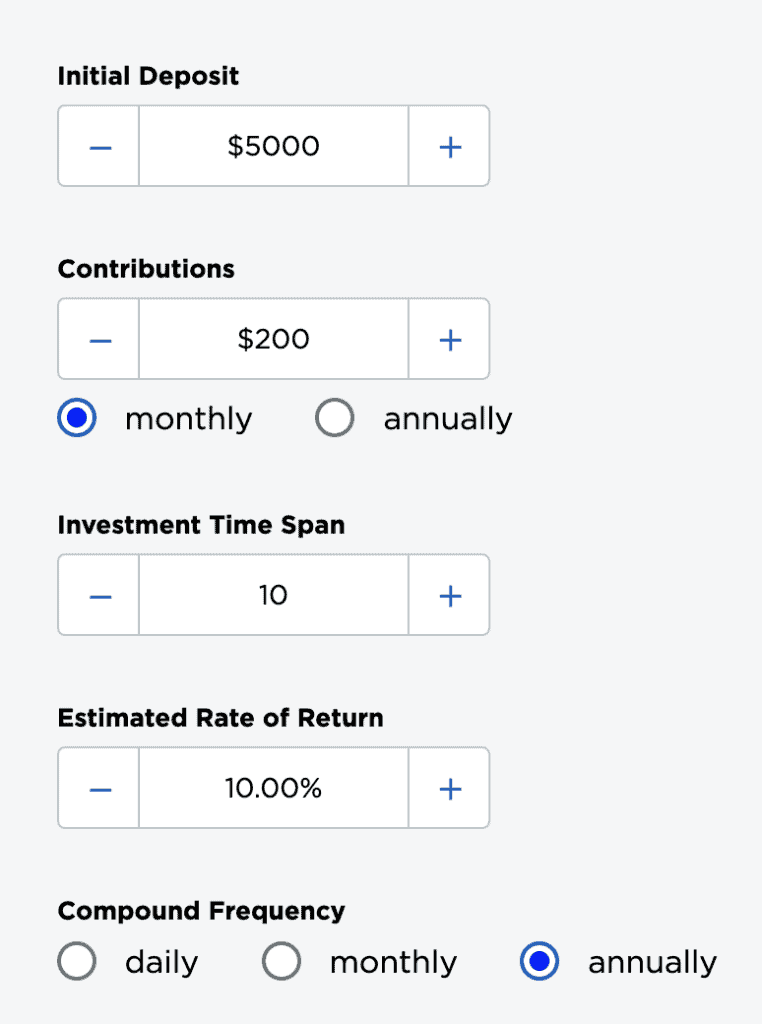

For example:

- If you invest $5000 in an normal brokerage (a business that trades stocks, indexes, etc)

- and then you add $200 every month for the next 10 years

- with an average interest rate of 10%.

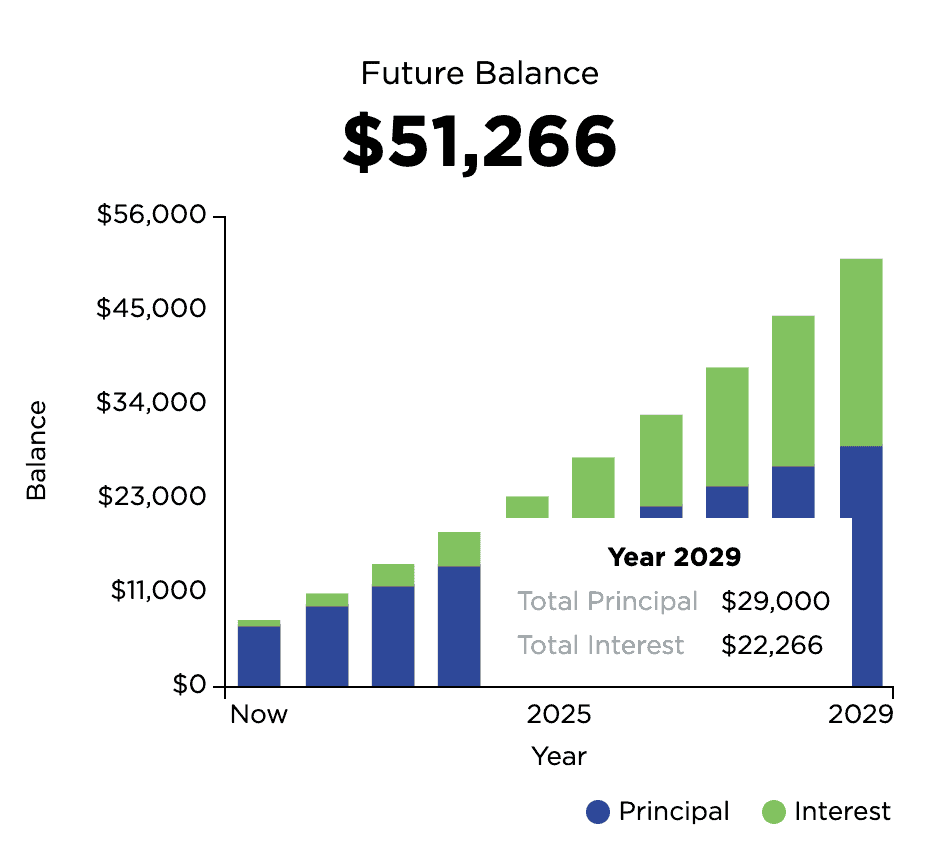

Your new balance – thanks to compound interest – is not $51,266!

You paid in (Total Principal) only $29,000 and that money then grew into $51,266 thanks to the additional $22,266 in reinvested interest!

If you’re a Gen Z and you’re only 20 years old, you’ll have that extra $22,266 in cash when you’re 30!!! We all hate and admire you at the same time lol.

Don’t believe me? Check out NerdWallet’s Compound Interest Calculator.

Gen Z Money Matters – Share & Save

As you can see, Gen Z Money is a force to be reckoned with. They are in the right space, at the right time, with access to food, money, and shelter thanks to their parents. There’s no shame in that.

Got questions? Follow me on Instagram! I’m a Millennial after all. DM & don’t be shy.

Read More Expat Money Tips:

- The Best Ways to Save Cash for Travel Quickly

- Investment Apps for Beginners You Need to Be Using

- Women: How Can You Start Investing?

- Review of MyExpatTaxes

Vanessa Wachtmeister is a travel tech professional and the creator of the wealth & wanderlust platform, Wander Onwards. Vanessa is originally from Los Angeles, California, she is a proud Chicana, and she has been living abroad for the last 9 years. Today, she helps people pursue financial and location independence through her ‘Move Abroad’ Master Class, financial literacy digital products, and career workshops.