Welcome to my Pink Money Series! Just as companies rebrand ordinary objects into pink ‘women-friendly’ alternatives, the Pink Money Series is where I explain money information with feminine colors so women know ‘it’s for us.’

Should You Start Investing Today as a Woman?

Should you start investing today? Well, that depends on who you ask. If you ask Cautious Cathy, she’ll warn you that ‘every investment is a gamble’ and that you’re better off keeping your money in the bank.

If you ask Bitcoin Betty, she’ll tell you that ‘crypto is the way of the future and that you should get in now.’

Investing is highly personal. Every individual tolerates different risk levels and long-term goals so there’s no one-size-fits-all recommendation.

You should be suspicious of anyone who prescribes you a ‘get rich quick’ strategy – even if they’re a certified financial advisor.

Before I continue, here’s my disclaimer: I am not a certified financial advisor. I cannot legally give you financial advice. Please don’t ask me to do so.

What I will be discussing is my own financial strategy, how I knew I was ready to invest, and specific scenarios that apply to my unique circumstances.

When I was Ready to Start Investing

My money journey officially started in 2015. I was £10,000 in debt, I was in school for my Master’s and working several odd jobs, and I felt like my life was out of control.

I ended up coming clean to my partner about how serious my debt was after we moved in together and it was the most embarrassing situation of my life.

He was very empathetic to my situation and never made me feel judged once… that’s probably why I married him a few years later!

Together, we drew up a budget and drew up a 6-month strategy, which utilized the ‘snowball‘ and ‘avalanche‘ debt payment methods.

In 6 months, I was debt-free!…. I was also hungry, deeply under-dressed for my age, and in need of a proper haircut, but DEBT FREE nonetheless.

In my opinion, the most important first step to start investing is clearing personal debt.

Need Some Help?

If you’re just starting out on your journey, check out my Beginner’s Budget Dashboard. It’s a Google Sheets template that tracks your expenses, income, investments, savings and more! There’s even a free video tutorial to help you get started.

Pull Together an Emergency Fund

Establishing an ‘Emergency Fund’ is the next step you should consider when preparing to start investing.

An Emergency Fund (EF) is exactly what it sounds like – it’s a pot of money, that you don’t touch ever, that is specifically designated to pay off any unexpected expenses that might pop up.

This could be anything from an unexpected car repair to cushioning the impact of unemployment.

In the #DebtFreeCommunity, you’ll hear that $1000 is a good place to start and I would agree. But in an ideal world, you should have at least 3 – 6 months’ worth of fixed expenses in the bank before you start investing.

Read my Emergency Fund article to find out why!

Clear Any Credit Card Debt

If you’re currently in credit card debt, investing should potentially take a back seat until that’s cleared.

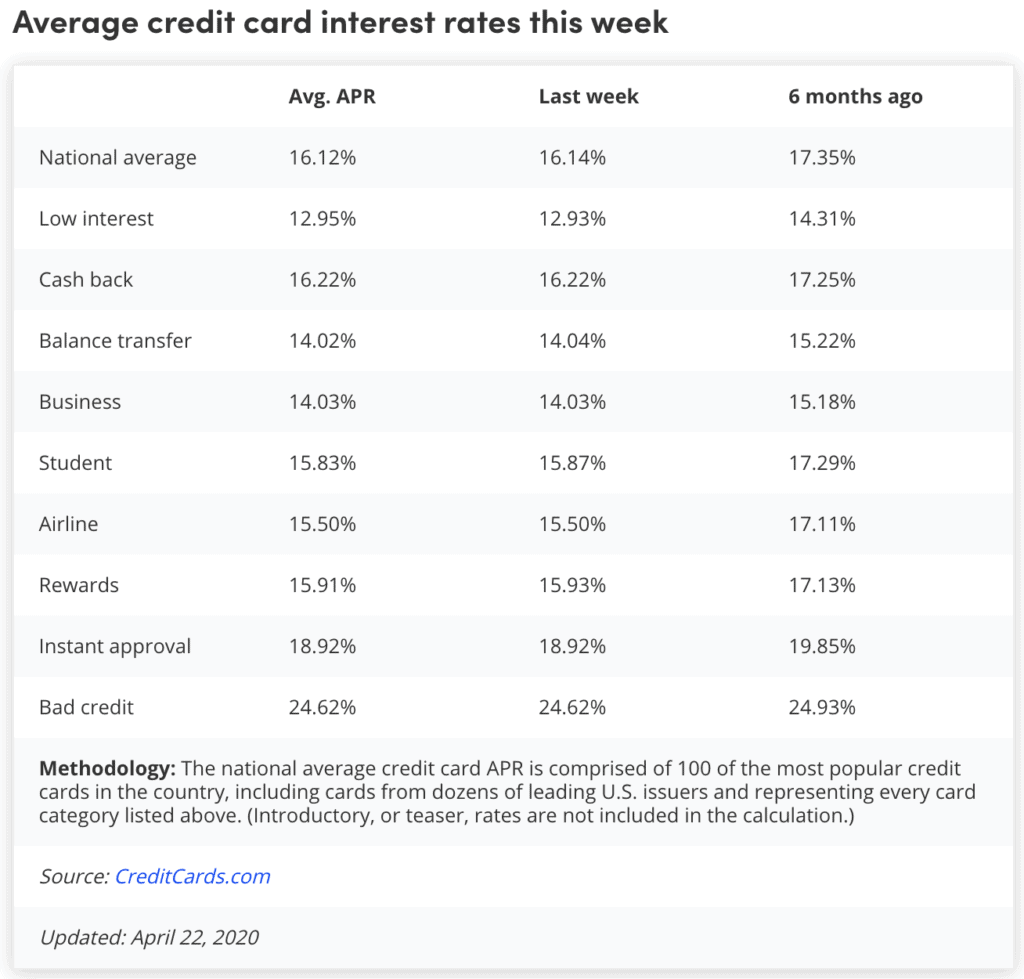

The average credit card APR (or interest) in America fluctuates around 16% according to creditcards.com and those with poor credit have been known to pay upwards of 24% interest!

If you’re in credit card debt, the interest that you pay on that debt will likely far exceed any immediate capital gains (or earnings from your investments) that you might make in the short run.

For example, if you have $10,000 in an Index Fund with an annual 7% return and $10,000 in credit card debt with an annual APR of 16%. By the end of the year,

- You earned $700 from your Index Fund investment

- You owe $1,600 to your credit card

That means you lost $900.

It’s the small print you want to be worried about. Passive investment options (like Index Funds or ETFs) typically won’t outearn aggressive credit card APRs so play it safe and focus on debt repayment first.

Pull Together a Plan B

With COVID-19 kicking us all in the ovaries, I knew that I needed a Plan B if I was going to start investing serious money.

Fortunately, I live in the United Kingdom and the Government is currently sponsoring 80% of furloughed employees’ salaries up to £2500 per month.

If you’re in America, this is likely not the same scenario so you’re going to want to figure out a Plan B of your own.

Some ideas include:

- Moving into smaller or more affordable accommodation

- Moving in with parents or family for free or subsidized rent

- Moving to a tier 2 or 3 city with a more affordable cost of living

- Taking up an additional side hustle or income source

- Making serious lifestyle concessions (like no more avocado toast??)

When you understand what you’re willing to do if the absolute WORST happens, you’re less likely to be terrified of the future. This is why we have Plan Bs!

Go beyond the money basics

Improve your mastery of budgeting, debt repayment, investing, and personal finance in just 6 weeks!

Determine Your Risk Level

Not all investments are considered equal. Typically, the more risky the investment, the higher the returns on investment….

BUT there’s also a higher risk of collapse.

If you’re financially responsible for immediate family members, aging parents, or anyone other than yourself, then you’re going to need to consider how struggling investments will impact your ability to support them.

For my family, we are double-income with no kids; or DINKs as the cool kids are saying. So we’re inclined to play it more ‘risky’ than we would 5 years from now if we have a young family.

It’s a very personal decision that each new investor needs to come to terms with.

Do Your Research

If you’re considering investing in the financial markets, take a look at how a stock, fund, or ETF has performed over the last 10 – 5 years to understand the average rate of return. For example, let’s look at my favorite Index – The S&P 500.

The S&P 500 is generally considered to be one of the best representations of the U.S. stock market.

As defined on Wiki, the S&P 500 ‘is a stock market index that measures the stock performance of 500 large companies listed on stock exchanges in the United States.‘

When the S&P is down, it’s a fair assumption that the economy is down too.

Indexes like this will give you a better understanding of how an industry is doing and what the average rate of return is. Unless you are swing trading, a good financial strategy should always take time into consideration as well.

Building wealth is a long-term goal; it’s not something you can do in a few short months typically. I would be dubious of anyone who disagrees with that logic.

Max Out Tax-efficient Options First

Investing may sound sexier than it actually is as most investors are normal people and not ‘Wolf of Wall Street’ characters. I can assure you that becoming an ‘investor’ has not made my life more or less glamorous; I’m just more intentional with my money.

Before you start investing, it’s important to understand how this will impact your taxable income.

For me, I am always interested in maxing out my ‘tax efficient’ before I start investing in anything else. ‘Tax-efficient’ options are investment allowances that either defer or are exempt from tax.

Investopedia explains:

Every investment has costs. Of all the expenses, however, taxes can sting the most and take the biggest bite out of your returns. The good news is that tax-efficient investing can minimize your tax burden and maximize your bottom line—whether you want to save for retirement or generate cash.

The reason I prioritize tax-efficient options first is:

- You lose any money you pay in taxes.

- You lose the growth that money could have created if it were still invested (damn).

This is because your after-tax returns matter more than your pre-tax returns.

In America, the popular options include:

Tax-deferred (upfront tax break):

You may be able to deduct your contributions to these plans from your taxable income, which provides an immediate tax benefit. Then, you eventually pay taxes when you withdraw your money in retirement—so the tax is “deferred.”

Tax-Exempt (After-tax dollars):

Because you’ve already paid tax on this money, your investments will grow tax-free and qualified withdrawals in retirement are tax-free as well. That’s why these accounts are considered “tax-exempt.”

In the United Kingdom, ISAs (Individual Savings Accounts) are the most popular tax-efficient options for individual investing.

Each individual is given an ISA allowance of £20,000 per financial year that is free from Capital Gains Tax. You are also allowed another £9,000 in allowance for a Junior ISAs (more below).

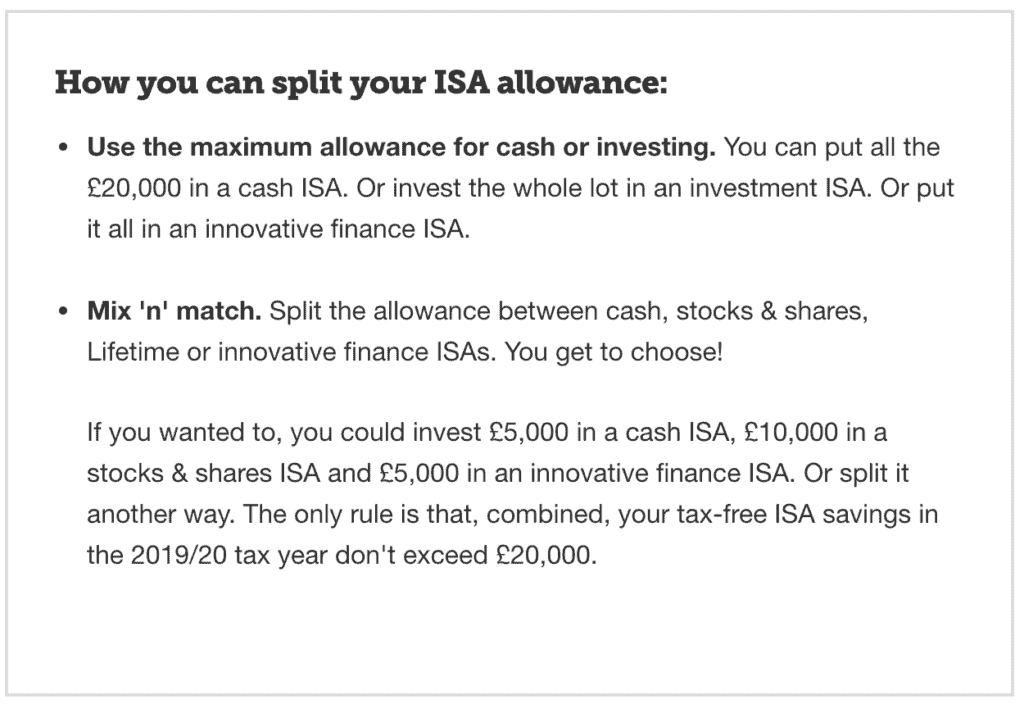

There are man mix’n’match options regarding how you can spend your £20,000 allowance. Read about ISA Options – here.

Stocks & Shares

Invest your ISA allowance in the stock markets.

Cash ISA

Variable or fixed rate of interest on a sum of money, usually over a set period of time. You are guaranteed this income, but interest rates are at all-time lows. (ex. 1.45% on up to £10,000)

Junior ISA

You can open a Junior ISA for your children with a £9,000 annual allowance.

Lifetime ISAs

£4,000 annual allowance, where the UK government adds a 25% bonus to anything you pay in, up to the age of 50. If you make withdrawals for anything other than to buy your first home or to fund your retirement, you pay a 25% charge.

You can split your allowance in a variety of ways, just make sure to do your reach search about what combinations are possible. (example below from Money Saving Expert).

Are You Ready NOW to Start Investing?

Like I said at the beginning. I am not a financial advisor. I cannot legally give out investment advice. Please consult a certified financial advisor before moving forward with any transactions as capital is at risk.

Nevertheless, I hope this article was helpful in your financial journey! It’s a very personal and LONG road ahead, but we all started somewhere. Now it’s your turn.

DM on Instagram if you have any questions or if you just want to say hello! @wanderonwards

Disclaimer: Reminder, this Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on wanderonwards.co or my Youtube channel – Wander Onwards – constitutes as a solicitation, recommendation, nor endorsement by Wander Onwards LLC or it’s owner. All Content on this channel is information of a general nature and does not address the circumstances of any particular individual or entity. Capital is at risk. Invest at your own risk.

Learn More about Finances for Expats:

- The Best Investment Apps for the UK

- How to Create More Than One Source of Income

- Ways to Build or Fix Credit

- Gen Z Money: Money Advice & Investing Tricks

- What Exactly is a Zero-sum Budget?

Vanessa Wachtmeister is a travel tech professional and the creator of the wealth & wanderlust platform, Wander Onwards. Vanessa is originally from Los Angeles, California, she is a proud Chicana, and she has been living abroad for the last 9 years. Today, she helps people pursue financial and location independence through her ‘Move Abroad’ Master Class, financial literacy digital products, and career workshops.